What Japan PM Sanae Takaichi signed in Hanoi

Three days, six documents, AUD 7.6 billion a year. Tokyo has decided where its capital goes next.

Sanae Takaichi spent three days in Hanoi from May 1 and left with six signed cooperation documents and a public commitment to lift Japanese investment in Vietnam to AUD 7.6 billion a year, with bilateral trade reaching AUD 91 billion by 2030. Bilateral trade ran at AUD 78 billion last year, so the trade target implies modest growth on the existing trajectory. The investment number is the one worth pausing on. At AUD 7.6 billion a year sustained, Japan is committing to deploy each year more than five times what Australia has built up in Vietnam across three decades. DFAT’s most recent published figure put cumulative Australian investment stock in Vietnam at AUD 1.38 billion as of December 2020.

1. What was actually signed

The Japanese and Vietnamese leadership signed six cooperation documents during the visit, covering space technology, information and communications, irrigation, climate-resilient infrastructure, low-carbon growth, and a critical minerals supply chain framework. These documents are not contracts where one side pays the other for a specific project. They are formal agreements that the two countries will work together in each of these areas, with the actual projects, funding, and timelines to be negotiated later. Hence, their significance is that once the two prime ministers publicly commit to an area, officials get the mandate to negotiate specific projects in it, and private companies pursuing deals in that area know they will receive political backing and faster regulatory approval.

Additionally, the two governments set a target of AUD 7.6 billion in annual Japanese investment into Vietnam and a AUD 91 billion bilateral trade target by 2030, meaning the combined value of all goods and services the two countries buy and sell to each other annually. They also committed to training 500 PhD-level semiconductor researchers by 2030, with Japan hosting roughly half, which matters because semiconductors are the chips inside almost every modern device and the countries that train the experts shape where the industry grows. In the near term, Japan’s Idemitsu will supply 4 million barrels of crude oil to Vietnam’s Nghi Son refinery, one of Vietnam’s largest fuel-processing plants.

2. Japanese companies have stopped betting on China

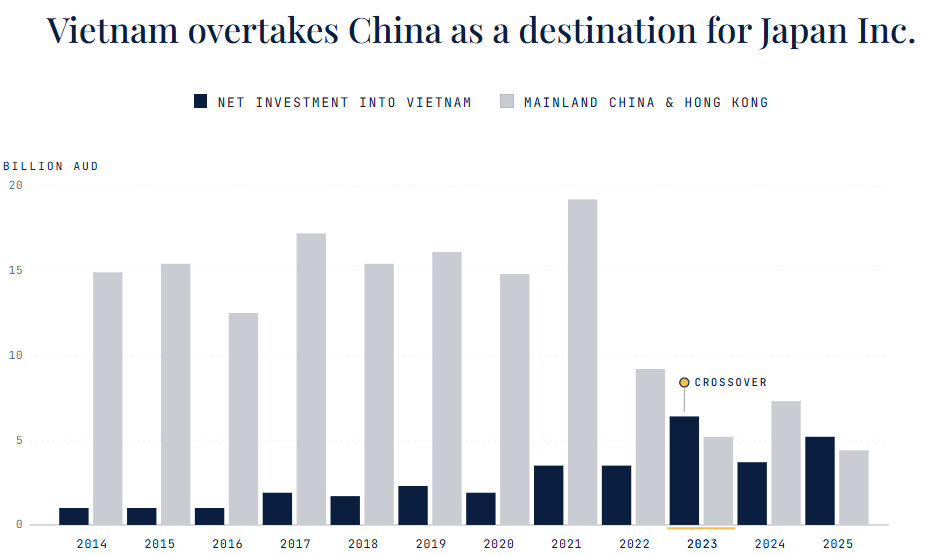

Net Japanese direct investment into Vietnam has overtaken net Japanese direct investment into mainland China and Hong Kong combined, with the crossover occurring in 2023. Japanese outbound capital into China has fallen from a peak of roughly AUD 14 billion in 2018 to under AUD 5 billion in 2025, while flows into Vietnam have risen steadily over the same period.

Takaichi made the underlying logic explicit in Hanoi, telling reporters that excessive reliance on specific countries for critical goods stems from unfairly low-priced supply conditions, and that strengthening supply chains requires fair competitive conditions based on factors other than price. She did not name China, but the framing left little ambiguity about which country she meant. The commitment she signed should therefore be read as the public ratification of a decision taken inside Japanese corporate boardroom several years earlier.

3. Japan has been here for years

The Takaichi commitment is credible because the deployment is already in market. Japanese institutions hold strategic minority stakes inside three of the four largest Vietnamese banks and the country’s largest insurer. The largest of those positions, SMBC’s AUD 2.3 billion for 15 per cent of VPBank in 2023, remains the biggest banking M&A transaction in Vietnamese history. Aeon operates one of the country’s largest shopping mall networks. Toyota, Honda, Canon and Panasonic run Vietnamese production facilities at a scale that has been quietly expanding as Chinese capacity has been quietly drawn down.

What Takaichi signed in Hanoi was not the start of Japanese deployment into Vietnam. It was the public confirmation of a position that Japanese capital has already taken.

4. So, what happens next

The first effect lands on Vietnamese banks that already carry Japanese capital. VPBank, Vietcombank, Vietinbank and Bao Viet Holdings have been operating with Japanese strategic shareholders for years. The Takaichi commitment turns those existing relationships into the obvious channels for the next wave of capital. New deals will not start from scratch. They will start from the positions Japanese institutions already hold.

The second effect lands on Vietnamese suppliers and joint venture partners. As Japanese factories continue migrating out of China, the local companies that supply them, lease land to them, and share equity with them all gain volume. This is the part of the agreement that does not appear in deal announcements but appears in earnings reports six to twelve months later.

The third effect lands on the ASX. A handful of Australian-listed companies already operate inside Vietnam. SunRice runs the Lap Vo rice mill in Dong Thap province. Blackmores has built consumer health distribution since the early 2010s. Austal has partnered on a Vietnamese shipyard since 2014. These positions were established when Vietnam was a small market for foreign capital, which means they were acquired at low entry valuations. As AUD 7.6 billion of Japanese capital flows in each year, the underlying Vietnamese market reprices upward, and the value of these existing Australian operations rises with it.

The fourth effect lands on future deal flow. Japan already holds strategic minority stakes of 15 to 20 per cent across three of the four largest Vietnamese banks, sits inside the country’s largest insurer, and operates the largest foreign retail and manufacturing presence. Any other foreign buyer entering Vietnam, whether Australian super funds, Korean conglomerates or European banks, must now compete in a market where Japanese institutions have already secured first-mover status across the most attractive assets. The question is no longer whether Vietnam is open for foreign capital. The question is what remains available after Japan.

Japan has built a position in Vietnam that no other foreign capital can match. Whether Australia eventually builds something comparable depends on what Australian capital does next.

Up next

The Australian leg of the Takaichi visit, including the prioritised commodity projects and the Japanese frigate contract. Published this weekend.

General commentary only. Not financial product advice.

Very well written!