Vietnam's AI Boom Runs on Power it Doesn't Have Yet

In Vietnam's AI build-out, the durable returns are in power, not chips, and Australia is selling the inputs instead of owning the assets.

1. Vietnam’s AI Ambitions Face a Stark US$18 Billion Infrastructure Reality

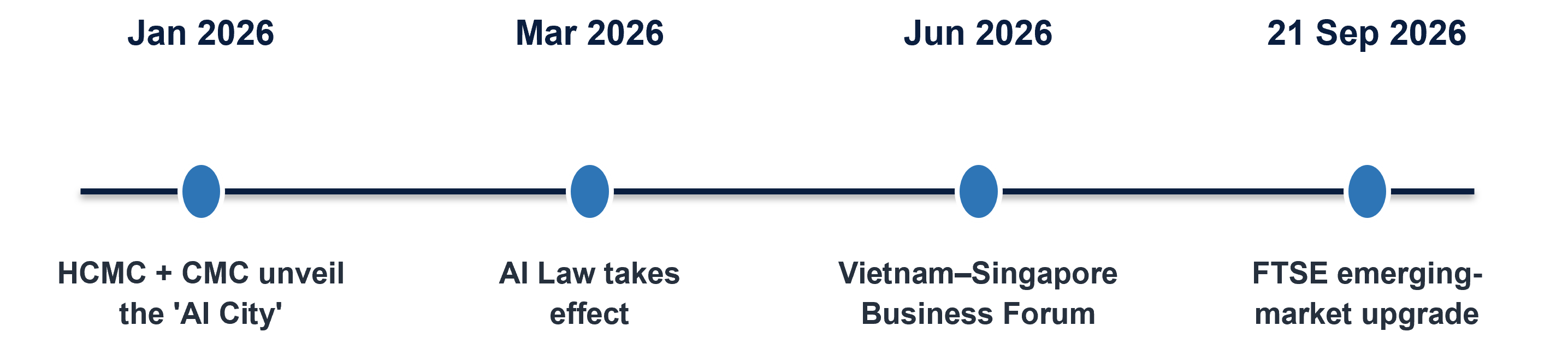

Vietnam’s push to become Southeast Asia’s next high-tech hub is accelerating. In January 2026, Ho Chi Minh City and the technology group CMC Corporation unveiled plans for what they call the world’s first ‘AI City,’ a model of centralised digital zones, chip-research centres and AI-driven urban governance. CMC has signed a parallel “triple-helix” partnership with the Hanoi People’s Committee and Hanoi University of Science and Technology to build an AI Centre of Excellence over 2026 to 2030. And in late June, the 2026 Vietnam–Singapore Business Forum tied rapid AI adoption directly to cross-border carbon markets and the next generation of green industrial parks.

These initiatives sit on top of a wave of global technology capital. Vietnam has secured more than US$7 billion in artificial-intelligence and data-centre commitments over the past two years. Samsung C&T and CMC are building a US$1.3 billion hub in Ho Chi Minh City, while Google and Alibaba plan to open their first hyperscale sites by 2027.

Yet as billions of dollars flow into software, smart cities and semiconductors, the entire boom runs into an unglamorous and deeply entrenched bottleneck: the electrical grid.

2. The immediate power strain

While city governments plan generative-AI assistants and smart-camera networks, the state utility Vietnam Electricity (EVN) is managing acute near-term capacity pressure. Driven by heavy industrial demand and the rollout of digital infrastructure, EVN has repeatedly warned of supply strain in the dry season, when depleted hydropower reservoirs and peak load collide.

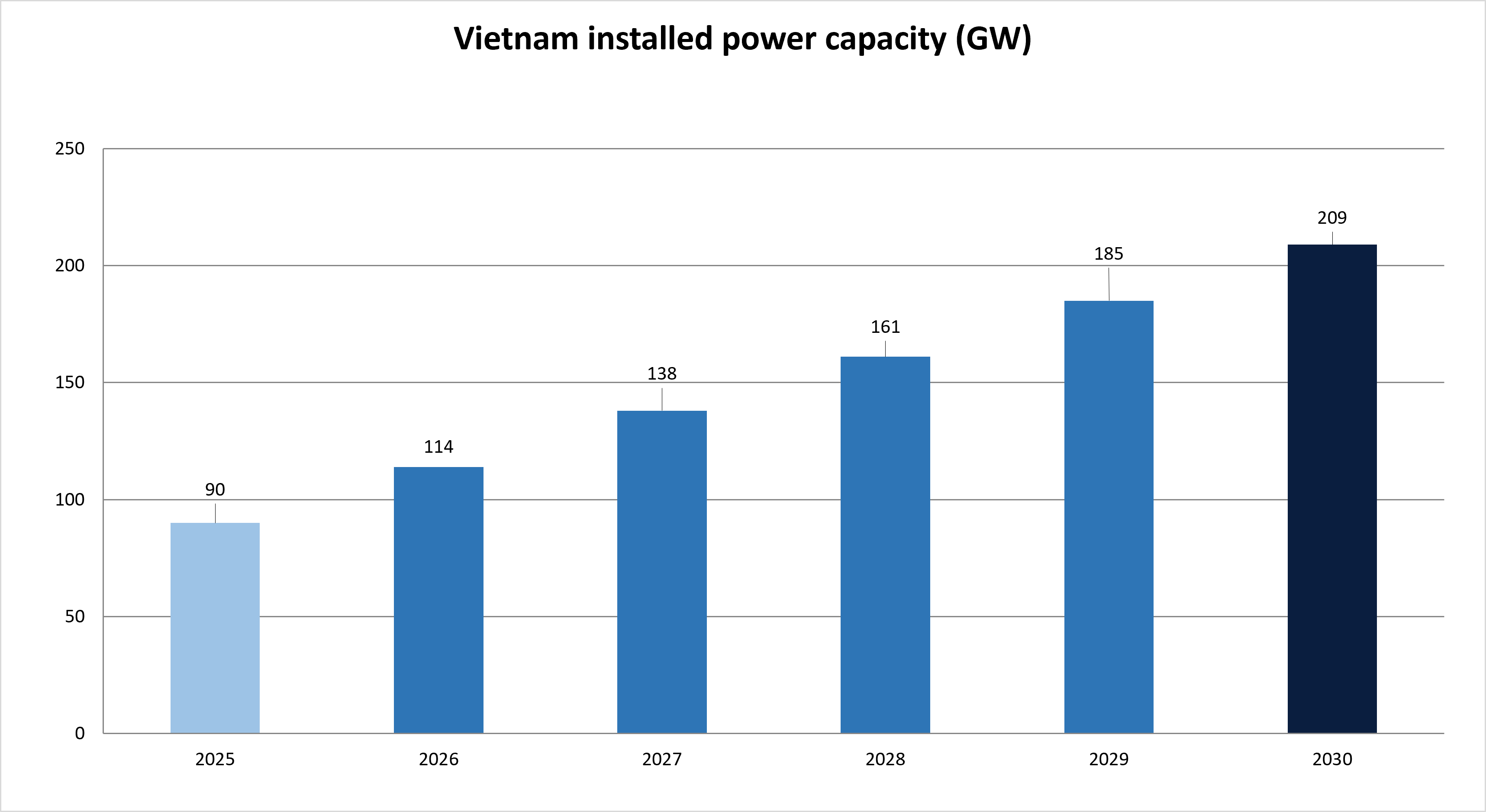

A data centre is, at its core, a facility that converts raw electricity into computing power. Vietnam ended 2025 with roughly 90 gigawatts of installed capacity, heavily anchored by coal and hydro. The government’s national power plan, PDP8, mandates expanding that capacity to between 183 and 236 gigawatts by 2030.

Hitting the target means building the equivalent of Australia’s entire electrical grid in five years, while national power demand climbs by as much as 15% a year. On top of that, the country must lay an estimated US$18 billion of transmission infrastructure this decade simply to move existing power from generation hubs to industrial centres.

Data centres themselves are projected to draw only about 1% of national demand by 2030. The constraint is not the volume of energy they consume but the type: AI facilities require firm, clean, round-the-clock power, and a grid leaning on coal and intermittent renewables cannot easily guarantee that continuous flow.

3. The long-term economics of infrastructure

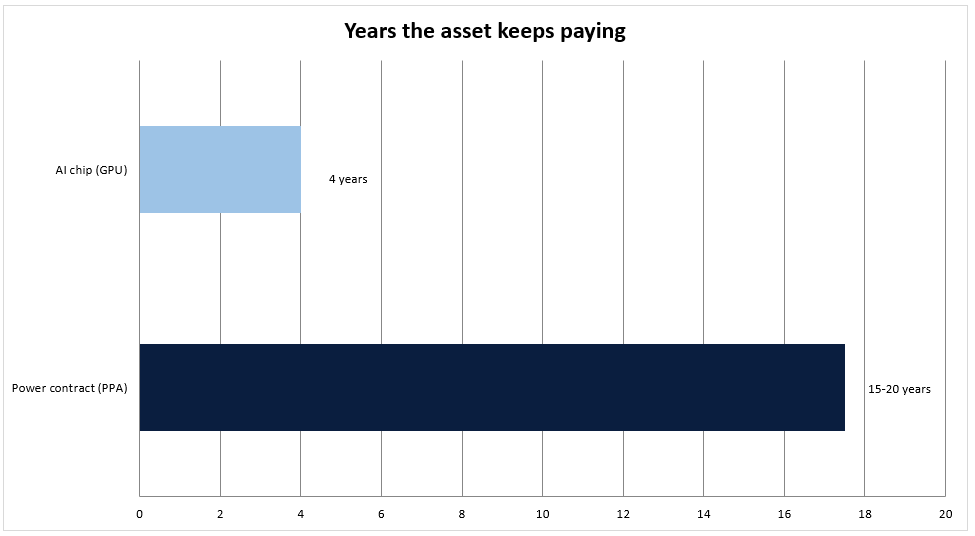

The economics of the AI build-out reveal a structural mismatch between technology assets and energy assets. High-end graphics chips depreciate quickly, often obsolete within four years. Because the hardware writes down so fast, the technology giants increasingly build their own hyperscale facilities rather than rent commoditised shells.

The power contracts beneath those facilities behave entirely differently. Because an AI data centre cannot pause when solar fades at dusk or the wind drops, operators secure guaranteed supply through contracts spanning 15 to 20 years.

Globally the pattern is well established: Google recently committed nearly US$5 billion to the clean-power developer Intersect, and Microsoft contracted nuclear output from Constellation Energy over 20-year terms. The hardware captures attention, but the long-dated power contract is the durable asset.

The computing power may generate the most excitement, but the 20-year power agreement is what provides durable value

4. The bankability gap

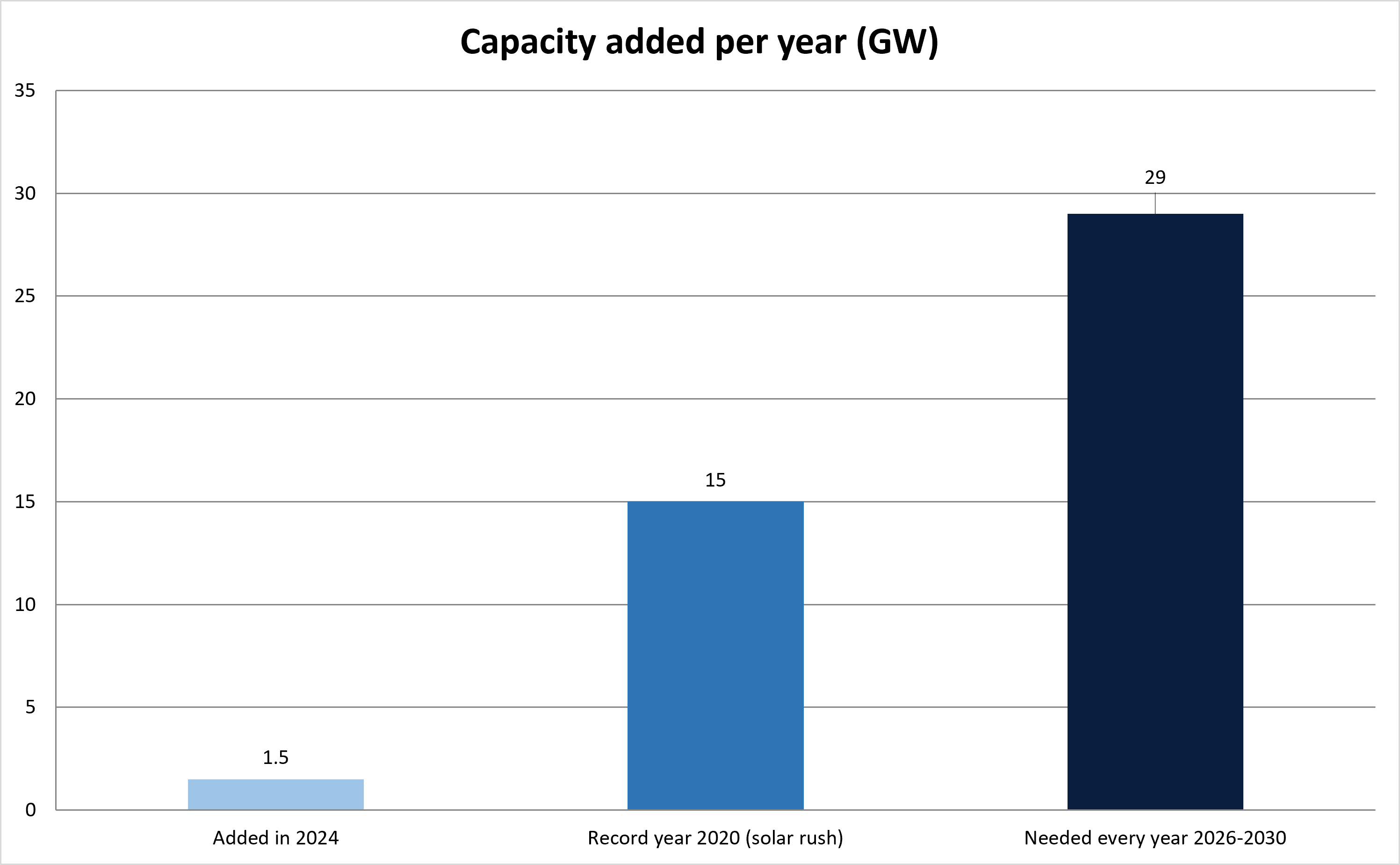

Building this infrastructure demands an extraordinary pace of execution. To meet the 2030 target, Vietnam must add up to 29 gigawatts of capacity every year. For comparison, its strongest year on record was a one-off solar rush in 2020 that added about 15 gigawatts; in 2024 the grid grew by just 1.5 gigawatts.

Financing multi-decade projects is the harder problem. EVN is the sole buyer of electricity in the country and carries a “BB” credit rating from Fitch, below investment grade and without a formal sovereign guarantee on its payments. Power-purchase agreements are settled in dong, creating substantial currency and convertibility risk over a 20-year horizon.

That environment explains why some international developers have recalibrated. In April 2026, Macquarie’s Corio Generation wound down its 2.5-gigawatt Vietnamese offshore-wind pipeline, having priced a long-term contract that standard project-finance lenders could not easily underwrite.

5. A mismatch in global capital

Vietnam’s energy challenge exposes how differently the world’s capital pools approach emerging-market risk. Japanese and South Korean institutions deploy through diversified trading houses, policy banks and life insurers, structures built to hold illiquid, long-dated assets for decades, the exact timeline a 20-year power contract demands. That lets consortiums from Tokyo and Seoul absorb counterparty risks other managers avoid.

Australian capital is built largely to originate and exit. Bound by strict bank-capital rules and benchmarked to liquid quarterly returns, the country’s superannuation funds face structural hurdles in holding long-term emerging-market infrastructure risk. Australian companies such as Woodside are active in the market, shipping liquefied natural gas to Vietnamese terminals, but supplying fuel is a short-term trade that ends when a cargo lands. Owning the generation and the grid is a permanent, generational position in a fast-growing market.

WHAT IT MEANS FOR AN AUSTRALIAN INVESTOR

The durable return is the 20-year power contract, not the data-centre shell or the LNG cargo

Capturing it needs a vehicle built to hold emerging-market risk for two decades, the model Japan and Korea already run

Australia has the gas (Woodside) and the capital (A$4.2 trillion in super); what it lacks is the holding structure

Until Western pension funds and institutions design dedicated vehicles to underwrite these 20-year infrastructure risks, the long-term returns of Vietnam’s power decade will keep accruing to Tokyo and Seoul, not to Sydney.

General commentary only. Not financial product advice.