Sojitz, Hanwa, JX Metals, Marubeni, Mitsubishi

Five Japanese trading houses just took positions in Australian metals. Plus eleven frigates the other way. AUD 11.67 billion, signed in a fortnight.

Cover photo: 2021 JS Mogami (FFM-1), Mogami-class frigateSanae Takaichi flew from Hanoi to Canberra on 3 May 2026 and signed a AUD 1.67 billion critical minerals package with Anthony Albanese the next day. Two weeks earlier, in Melbourne, defence ministers Shinjiro Koizumi and Richard Marles had already signed the AUD 10 billion contract for three Mogami-class frigates that anchors the SEA 3000 program. Both events together mark the most consequential bilateral with Japan since the 1976 Basic Treaty of Friendship and Co-operation.

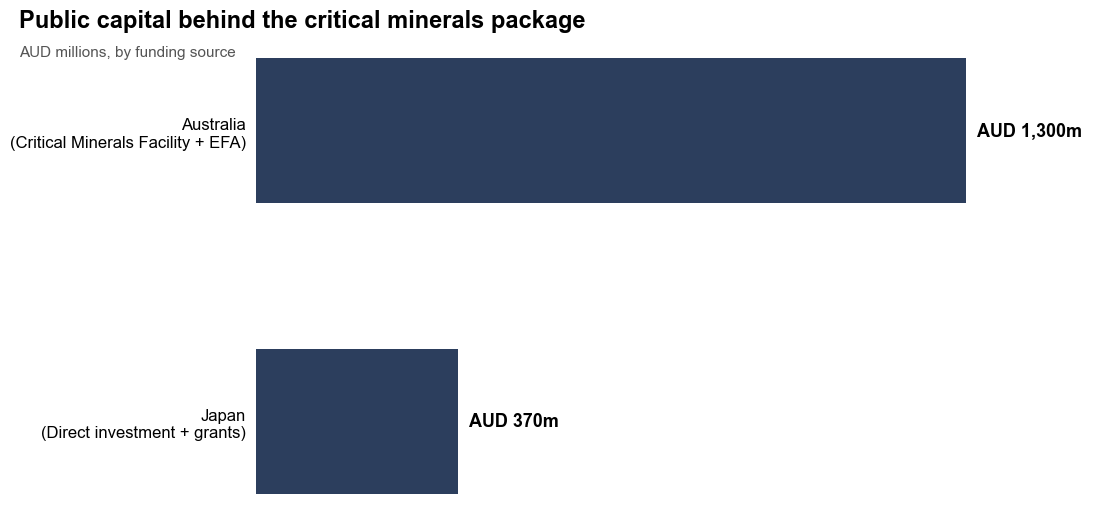

The number worth pausing on is the split. Australia put up AUD 1.3 billion through the Critical Minerals Facility and Export Finance Australia. Japan put up AUD 370 million in direct investment and grants (PM&C, 4 May 2026).

Australia is funding the production capacity. Japan is locking in the offtake, and the 3.5-to-1 split is the price Canberra is paying to become Tokyo’s long-dated supplier.

1. Public capital from Canberra, offtake from Tokyo

Two documents. The Australia-Japan Joint Declaration on Economic Security Cooperation is the umbrella. Underneath it sits the Joint Statement on Elevated Critical Minerals Cooperation, which is where the project list and dollar figures live. The PM&C release names six projects and confirms the structure: Australia carries the public capital, Japan supplies the technical partners and the offtake demand.

That structure matters. Australia is not selling raw ore. The agreement explicitly targets midstream processing. The plan is to turn concentrate into separated metals and chemicals inside Australia, with Japanese engineering and Japanese offtake locked in by long-dated contract. The release names JOGMEC (Japan Organization for Metals and Energy Security) and Export Finance Australia as the operating institutions. This is the same playbook Japan used on liquefied natural gas in the 1970s: lock in long-dated supply by financing the upstream infrastructure. Forty years later, Japan is still the foundation buyer of every major Australian LNG project. The minerals declaration is built on that template.

2. The six projects, and why these six

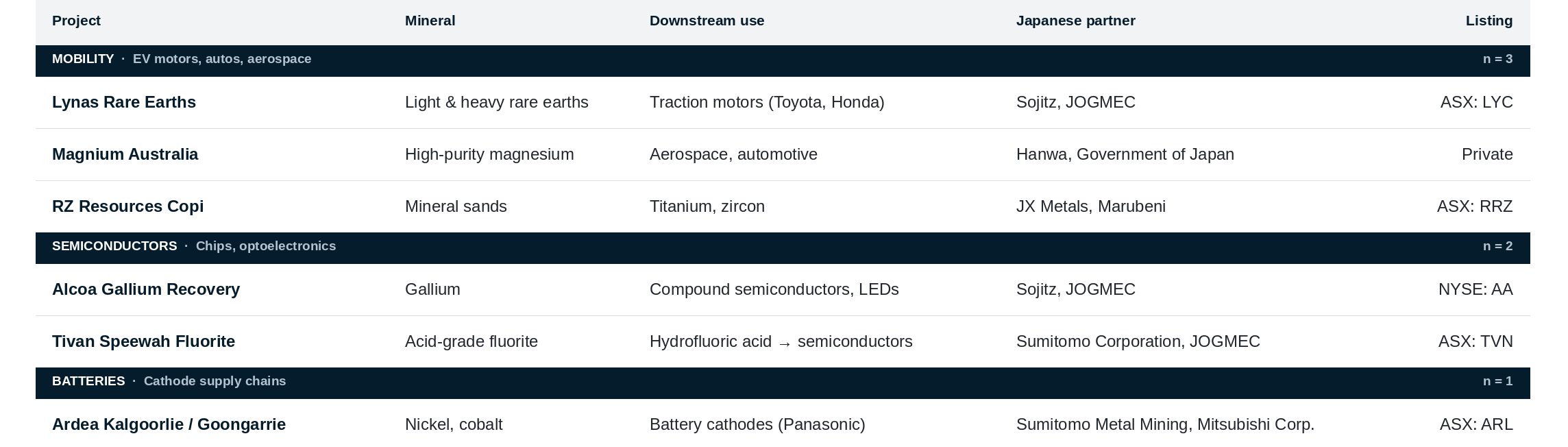

What follows is not Australia’s six largest critical minerals projects. It is the six where a Japanese industrial customer sits at the end of the supply chain:

Fluorite makes hydrofluoric acid, which makes semiconductors. Gallium goes into compound semiconductors and LEDs. Rare earths go into traction motors for Toyota and Honda. Nickel and cobalt go into battery cathodes for Panasonic. The list is engineered to plug specific holes in Japanese supply chains that, in 2026, all still run through China for at least one processing step. The point is to remove that step.

The institutional split is worth reading carefully. JOGMEC takes equity. Sumitomo Corporation, Sumitomo Metal Mining and Mitsubishi take operating roles. Export Finance Australia issues non-binding Letters of Support to the project companies. The structure means the Australian public balance sheet sits behind the projects but the Japanese commercial balance sheet sits inside them. That is the model Japan exported to Indonesia in coal in the 1980s and to Vietnam in power generation in the 2000s. It is now being exported to Australia in metals.

3. The frigate contract did not need a Prime Minister to sign

The Mogami Memorandum was signed aboard the JS Kumano in Melbourne on 18 April 2026, two weeks before Takaichi landed. Mitsubishi Heavy Industries will build the first three upgraded Mogami-class frigates in Japan. Vessels four through eleven are planned for the Henderson Defence Precinct in Western Australia. First delivery is 2029. Total program value sits at up to AUD 20 billion over a decade (Defence Ministers’ release, 18 April 2026).

Two things to register. First, the headline AUD 10 billion figure is for the first three hulls only. The total SEA 3000 envelope is twice that, and the Australian-built tranche carries the larger share of industrial workshare. Second, the deal is Japan’s largest defence export since Tokyo lifted its post-war export ban in 2014 (Japan Times, 18 April 2026). Australia is the first non-US partner to receive Japan’s fully weaponised platform: 32 vertical-launch cells, Tomahawk-capable. The Indonesian variant under negotiation gets 16 cells (Asia Times, May 2026). The differential is deliberate.

That the contract was signed before the Prime Ministerial visit, not during it, is the analytically interesting part. Takaichi did not arrive in Canberra to negotiate a frigate deal. She arrived to ratify one already done at the ministerial level and to bundle it with the minerals declaration into a single public moment. The choreography is the message.

4. Production end, not assembly end

Most coverage frames Takaichi visit as defence-plus-minerals. The throughline is narrower than that. Australia in May 2026 became the first foreign country to host both Japan’s largest postwar arms export and a sovereign-grade critical minerals partnership in the same fortnight. Vietnam, on the same trip, received six cooperation documents and an investment commitment of AUD 7.6 billion a year (METI joint statement, 1 May 2026), but no frigates and no minerals processing money. Indonesia gets a smaller Mogami variant and no minerals package. South Korea gets neither.

The position Japan is building in Australia is structurally different from what it is building anywhere else in the region. The Australian leg is the production end of the system. Vietnam is the assembly end. That is the architecture worth tracking, and it is not yet visible in the headlines from either capital.

The follow-on question is the one the Australian listed names will answer. Five of the six named partners (Lynas, Alcoa, Tivan, RZ Resources and Ardea) now have non-binding Letters of Support from Export Finance Australia. Magnium remains the only private participant. The next disclosure cycle, starting with the FY26 full-year results in August 2026, will show whether those letters translate into binding offtake, equity injections, or final investment decisions. Until those documents land on the ASX, the AUD 1.67 billion headline is a signal of intent. Japan has signalled intent before. In LNG, the signal turned into 40 years of dominant offtake. The minerals declaration is structured to do the same thing.

Japan is not selling Australia frigates and buying Australian minerals because it has to. It is doing both because it has decided what kind of partner Australia is going to be for the next 40 years.

General commentary only. Not financial product advice.